Berkshire, Progressive Are Underwriting Profit Leaders; Industry Sets Income Record

S&P Global Market Intelligence expects the U.S. property/casualty insurance industry to post more than $100 billion of net income for 2024—and that the biggest underwriting profits contributing to the figure will come from units of Berkshire Hathaway and Progressive.

{kind=link}

The triple-digit aggregate industry net income figure will come from a combination of sharply improved underwriting results, for personal lines, in particular, coupled with the positive effects of higher interest rates on investment income, S&P GMI said in a new report based on data compiled from property/casualty annual statement filings with the National Association of Insurance Commissioners as of March 6.

This would mark the first time in a calendar year that the industry posted net income over $100 billion, the report said, noting that the net income figure compares to $85.1 billion for 2023.

Estimating an overall combined ratio of 96.6 for 2024, compared to 101.8 for 2023 and 102.7 in 2022, S&P GMI said the industrywide underwriting profit will total almost $27 billion. “An approximate year-over-year swing of $47 billion from the industry’s second-consecutive net underwriting loss in excess of $20 billion” for the two prior years “has few historical precedents,” according to Tim Zawacki, insurance sector strategist at S&P Global Market Intelligence.

[inline-ad-1]

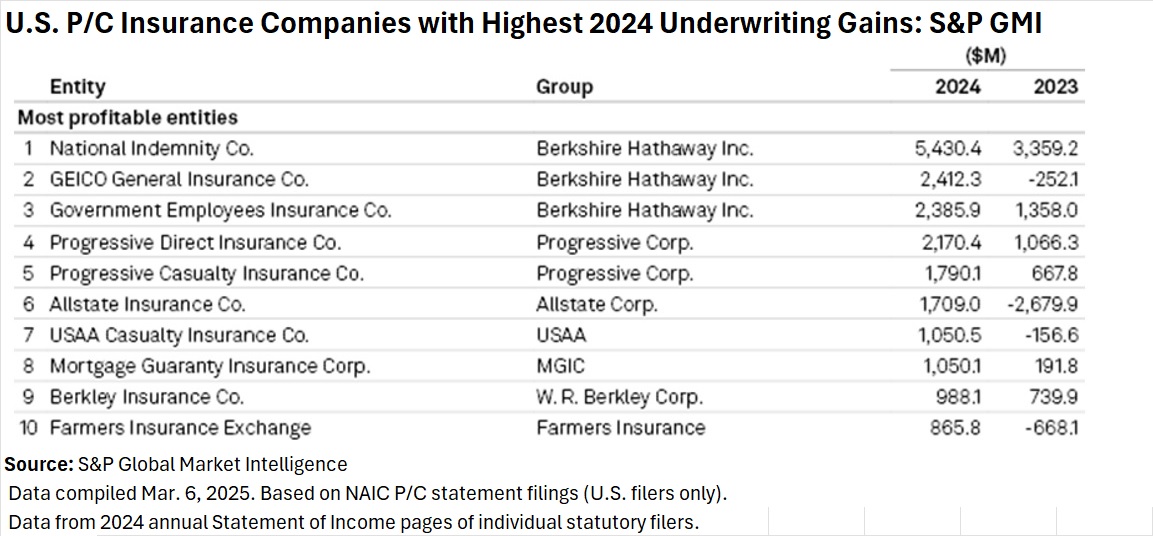

Ranking individual insurance companies based on underwriting profit, S&P GMI found that three U.S. P/C subsidiaries of Berkshire Hathaway Inc.—National Indemnity Co., GEICO General Insurance Co. and Government Employees Insurance Co.—were the industry’s most profitable individual entities, while Berkshire Hathaway Group overall recorded $12.2 billion of net underwriting profits on a statutory basis. (Individual company results are shown net of reinsurance, and National Indemnity’s results include a boost from reinsuring GEICO business, the report notes.)

Related article: Polished Gem GEICO Fuels Berkshire Hathaway Operating Gains

Seven of the insurers showing the largest underwriting profits write primarily personal lines, including two Progressive entities—Progressive Direct Insurance Co. and Progressive Casualty Insurance Co.—along with Allstate Insurance Co., USAA Casualty and Farmers Insurance.

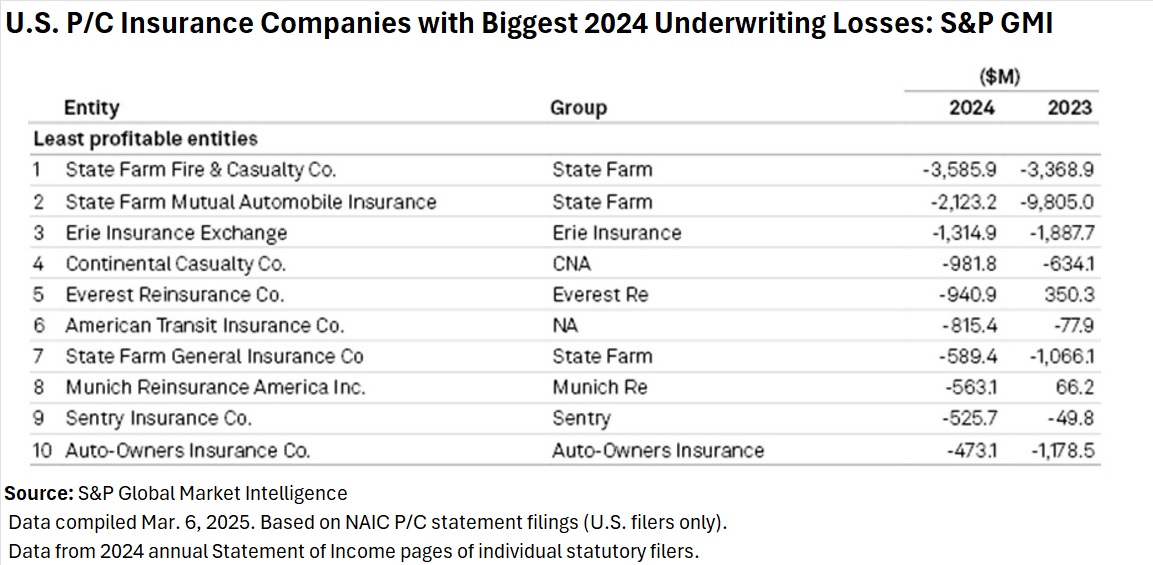

But writing personal lines wasn’t the secret sauce to move to underwriting profitability last year. While State Farm Mutual Automobile Insurance Co.’s net underwriting result improved the most of any insurer captured in the S&P GMI analysis, even with a $7.7 billion improvement the company still reported net underwriting losses of $2.1 billion, according to S&P GMI. That was the second-worst underwriting result in the industry, topped only by another State Farm entity—State Farm Fire and Casualty Co.

{kind=link}

California-focused State Farm General Insurance Co. had the seventh-largest underwriting loss last year.

Related article: State Farm Stronger as Underwriting Losses Shrink—But Not in California

Commercial lines trends marred results for companies like Everest, with adverse prior-year reserve development contributing to a $1.3 billion swing in underwriting results—the biggest dollar-deterioration tallied by S&P GMI.

Related articles: Everest Group Boosts Casualty Loss Reserves $1.7B; ‘Underwriting Choices’ Added to Everest’s Social Inflation Woes: CEO

The report includes a graph with combined ratios—and the loss, expense and dividend ratio components—for each year dating back to 2014, along with discussions of loss ratio changes by segment and the impacts of catastrophe losses. Another graph reveals dollars of net U.S. P/C underwriting gains and losses for each year dating back to 2000.

Overall, the combined ratio swing to 96.6 last year from 101.8 in 2023 marks the most significant year-over-year reduction since 2013, the report notes.

Even though 2024 was a heavy year for natural catastrophes, significant loss amounts from severe convective storms and third- and fourth-quarter hurricanes flowed onto the books of reinsurers that are based outside of the United States and were therefore not included in the results reported by S&P GMI. In addition, the report noted that a material portion of losses from Hurricane Helene were caused by floods and not covered under typical residential property insurance.

Looking ahead, the report suggests that in spite of the January wildfires in California, S&P GMI expects the industry to experience another year of strong underwriting profit in 2025 given the profit momentum in the private auto business.

The profit and loss figures and ratios tabulated for 2024 are based on data available through the beginning of March, according to the report, which notes that while the results may change to some extent as additional information becomes available, the S&P GMI researchers do not believe that the outstanding filers are individually or collectively significant enough to dramatically influence particular line items.

- Jury Awards 78-Year-Old Victim $56 Million for Crash Caused by Amazon Delivery Driver

- Chobani Must Face Lawsuit Over Zero-Sugar Yogurt Claim, Appeals Court Rules

- Why El Niño’s Promise of Quieter Hurricane Season May Not Be Good News for Insurers

- Zurich CEO Says Staff Let Go as Regulator Finma Imposes Partial Sales Ban