Tesla Premiums Soared in 2025 With Loss Ratios Worse Than Industry

While auto insurance leaders reported premium growth percentages in the single digits last year, with sprinters like Progressive and Root up in the low-to-mid teens, premiums at Tesla’s insurance operations skyrocketed 40.7%, according to a new analysis.

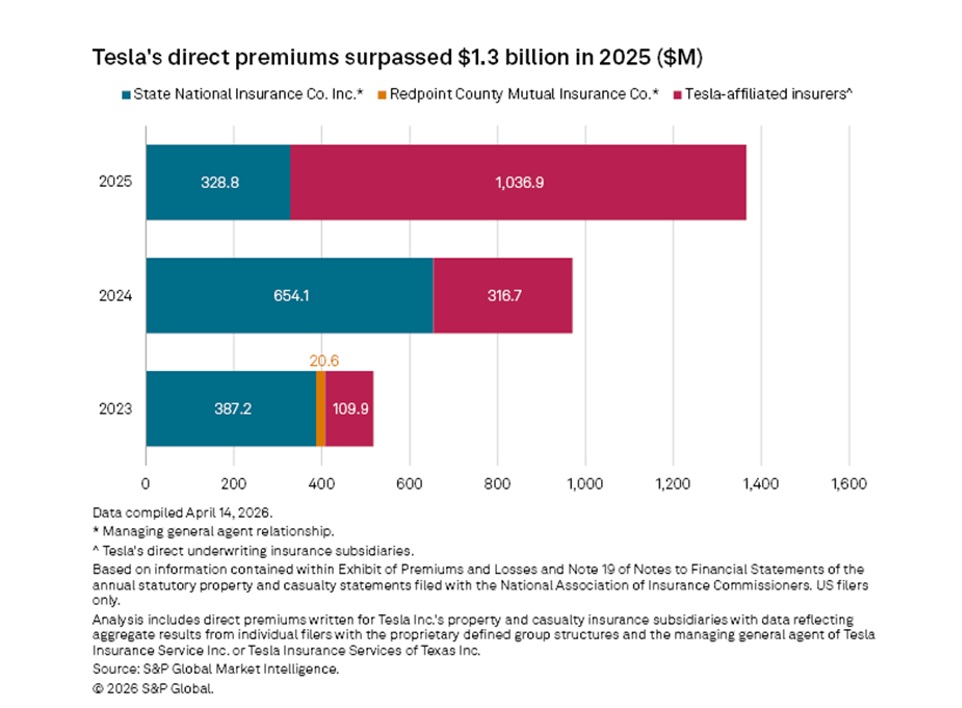

S&P Global Market Intelligence reported total direct premiums across Tesla’s insurance business topped $1 billion last year, coming in at nearly $1.4 billion, compared to $970.8 million in 2024.

But while Tesla’s premiums soared—particularly in California, where a whopping 585% jump brought the state’s premiums to $725 million, compared to just over $100 million in 2024—loss ratios for one of the Tesla insurers, Tesla Insurance Co., continued to look worse than an industrywide combined ratio in 2025.

{kind=link}

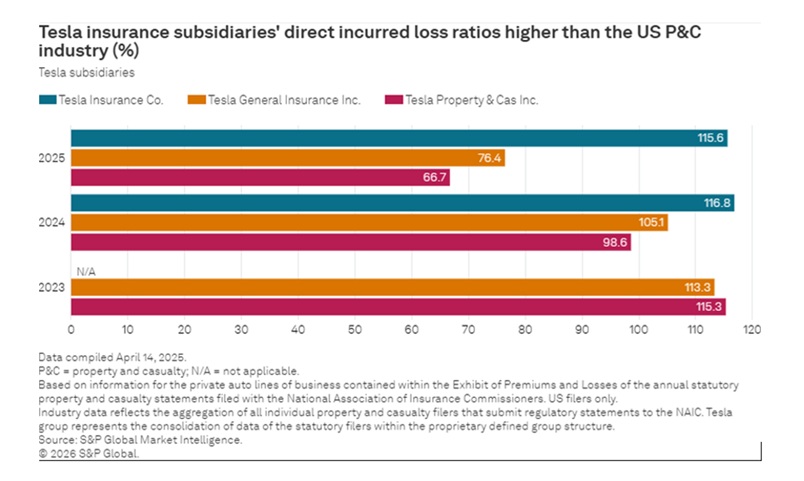

According to a chart included in the S&P GMI report, the direct loss ratios for Tesla Insurance Co. exceeded 115 in both 2025 and 2024.

There are three Tesla carriers for which key metrics are captured in the report: Tesla Insurance Co., Tesla General Insurance Inc. and Tesla Property & Casualty Inc. Among them, Tesla Insurance Co. is currently the principal writer of California business, S&P GMI confirmed, supplying information that shows 100% of Tesla’s California premiums in that company.

In addition, Tesla Insurance Co. is also one of two Tesla insurance entities in the state of California flagged for improper claims handling by the California Department of Insurance last year. Announcing actions against the companies, CDI threatened to enforce monetary penalties and to suspend the certificate of authority of insurer Tesla Insurance Co. to transact insurance business in California, and to revoke the license of broker Tesla Insurance Services. Tesla Insurance Services has acted as a general agent for Tesla Insurance Co. in California, and for a non-affiliated insurer, State National, a member of Markel Group.

S&P GMI highlights a change in the relationship between State National and Tesla as the driver of the surge in premiums across the Tesla insurance subsidiaries.

According to S&P GMI, State National Insurance Co.’s share of Tesla’s insurance business shrank to 24% in 2025 from 85% in 2022, following Tesla’s 2023 offer of a one-time 5% discount for customers to switch carriers.

{kind=link}

With the business successfully transitioning from the Markel fronting carrier to Tesla’s direct underwriting operations, Tesla’s affiliated insurance company premiums across all states grew 227.4% to just over $1 billion ($1.036 billion) in 2025 from $316.7 million in 2024, representing nearly 76% of the $1.3 billion total.

Highlighting “a strategic shift away from managing general agents,” S&P GMI notes that State National’s share of the Tesla premium pie was almost cut in half—falling to $328.8 million in 2025, compared to $654.1 million in 2024.

Offering further insight on state-by-state writings, S&P GMI notes that while the off-the-charts growth in California now puts the state’s share of all premiums written by Tesla affiliates at 70%, Tesla’s growth in second-ranked Texas was roughly 16%. In 2024, California and Texas each accounted for roughly one-third of the $316.7 million total premiums written directly by Tesla affiliates.

Geographic expansion accelerated significantly in 2025, with Tesla entering four new states: Arizona, Ohio, Illinois and Florida, collectively writing $43.3 million in direct premiums. Nevada demonstrated the second-largest growth rate at 89.2%, increasing from $22.5 million to $42.5 million in direct premiums written, S&P GMI noted.

Nevada is one of four states written out of Tesla General Insurance Co., representing more than 40% of the company’s total premiums, according to supplemental information S&P GMI supplied to Carrier Management.

The report includes a graph of premiums written in 2024 and 2025 in all three Tesla companies combined by state for 13 states where they write auto insurance.

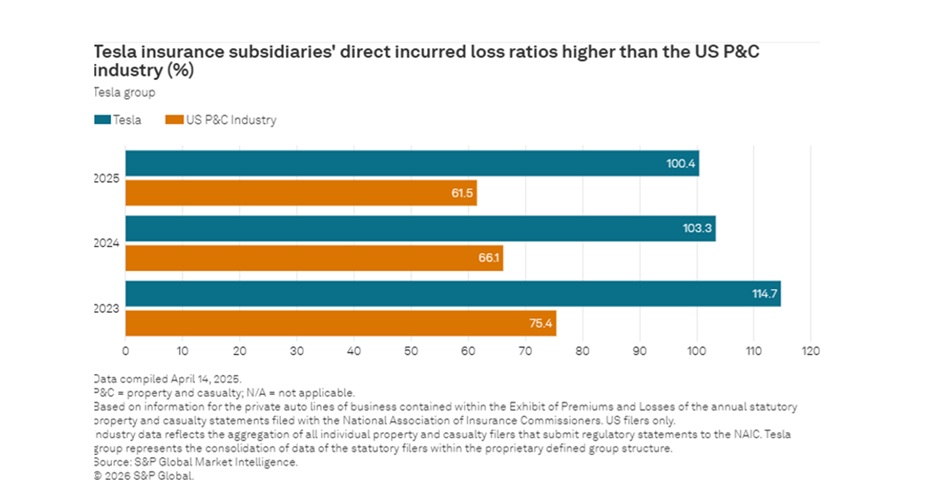

On the loss ratio front, Tesla’s insurance carriers reported an overall direct loss ratio of 100.4, almost 3 points better than 103.3 in 2024. But the gap between Tesla and the P/C industry as a whole has stayed near 40 points for the last three years, a chart in S&P GMI’s report revealed (copied below).

{kind=link}

Individually, Tesla Property & Casualty has experienced the most loss ratio improvement in the last three years—dropping to a direct loss ratio of 66.7 in 2025 from 115.3 in 2023. Tesla P&C wrote in seven states last year, with Texas representing 60% of the company’s total direct premiums, according to information S&P GMI shared with Carrier Management.