Strong Underwriting, Investment Income Bolster P/C Income in 2025, Says Moody’s

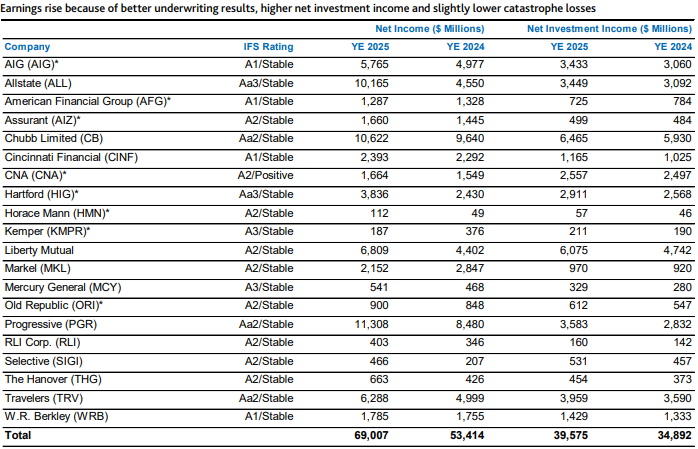

Twenty insurers rated by Moody’s reported net income of $69 billion in 2025, up 29% over 2024, as the combined ratio for the group improved in 2025 to 88.4 from 91.7 the prior year.

Losses from the Los Angeles wildfires early in the year were somewhat offset by no landfalling hurricanes for the first time in a decade, as well as fewer losses from severe convection storms, to drop overall catastrophe losses for the rated companies 9% to $19 billion in 2025.

{kind=link}

Personal auto insurers in the group, using rate increases approved by state regulators over the last several years, improved profitability. The 2025 auto combined ratio for a sample of seven insurers—Progressive, GEICO, Allstate, Travelers, Kemper, Hartford, and Horace Mann—improved 2.2 points to 86.4.

Moody’s said it expects “increased competition amongst personal auto insurers in 2026 as many of them are focused on growth in policies-in-force.” Net premium written for the sample group increased 10.3% to about $170 billion in 2025, but rate increases during the year were lower than previous years, with some insurers decreasing rates to grow market share, Moody’s added.

Meanwhile, a sample of five homeowners insurers—Allstate, Travelers, Progressive, Hartford, and Horace Mann—turned in an aggregate combined ratio for 2025 of 86.2 versus 92.3 for 2024. Net premiums increased 10.4% to about $30.3 billion.

Like in homeowners, commercial property rates declined in 2025. Competition drove rate decreases of 9% and 8% in the second two quarters of 2025, respectively. Commercial P/C insurers increased casualty lines prices, which Moody’s said will drive continued underwriting profitability in 2026 for commercial insurers.

{kind=link}