US P/C Insurance Industry Income Tops $100B in 2024: Verisk, APCIA

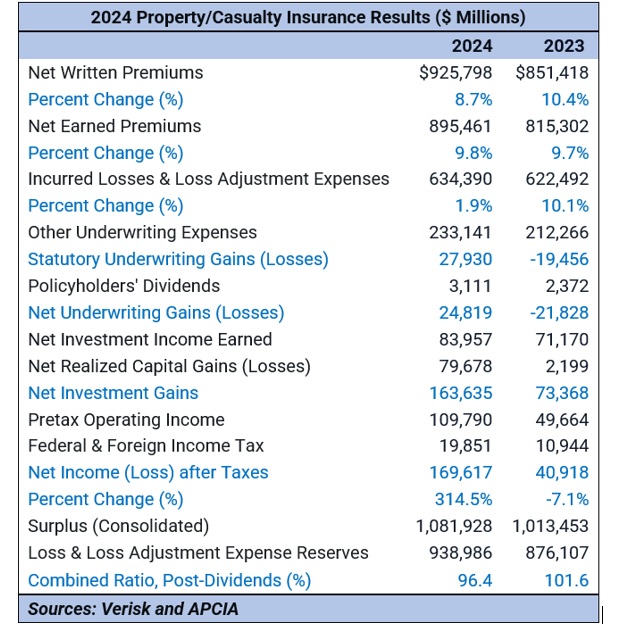

The U.S. property/casualty insurance industry reported its first full-year underwriting gain in four years, fueling a jump in net income to $170 billion, according to a joint report from Verisk and The American Property Casualty Insurance Association (APCIA).

The global data analytics and technology provider and insurance company trade association noted that the net income figure included $70 billion from capital gains realized by insurers in Berkshire Hathaway group. Excluding that hefty investment gain for one enterprise, full-year 2024 net income is estimated to be $100 billion for the industry overall.

Anticipating the $100 billion-plus figure last week, S&P GMI reported that this marked the first time in a calendar year that the industry posted net income over $100 billion.

Both the S&P GMI and the Verisk/APCIA reports highlight a swing in underwriting results—moving from a net underwriting loss of more than $20 billion in 2023 to an aggregate industry net underwriting profit of more than $20 billion in 2024. Specifically, the Verisk/APCIA report puts the 2024 underwriting gain at $24.8 billion, compared to a $21.8 billion underwriting loss for 2023.

{kind=link}

“While many of the loss drivers of 2023 persisted into 2024, the industry’s ability to bring premiums closer to the requisite levels has led to an underwriting gain for the first time since 2020,” said Saurabh Khemka, co-president of underwriting solutions at Verisk, in a statement.

Net written premiums overall jumped 8.7% to $926 billion in 2024, compared to $851 billion in 2023. Earned premiums grew 9.8% to $895 billion.

The combined ratio improved to 96.4 in 2024, down more than 5 points from the 101.6 aggregate industry figure recorded for 2023.

Related: AM Best: US P/C Industry in 2024 Posts First Underwriting Profit in Four Years

Khemka noted necessary premium adjustments in personal auto, in particular, drove improved results for personal lines. “While commercial auto premiums followed a similar trend, its growth rate did not match the levels seen in 2023,” he said.

Among challenges that continue to fuel losses for the industry are property catastrophes, Khemka said, noting that last year marked the second worst year for catastrophic losses since 1950.

“Most notably, Hurricane Milton, along with a series of late-season storms, drove fourth-quarter catastrophe claims to surge 113% higher than the same period in 2023, highlighting both the volatility and financial strain insurers face,” he said.

Robert Gordon, senior vice president, policy, research and international at APCIA, took note of continuing catastrophes in 2025. “By this time next year, homeowners insurers will have likely reported seven consecutive years of net underwriting losses, including record insured losses caused by the California wildfires this January,” he said.

In spite of the catastrophe losses in 2024, the four-fold jump in net income (including the investment gains recorded for Berkshire’s National Indemnity, National Fire and Marine, and Columbia Insurance Company) helped push policyholders surplus up to nearly $1.1 billion.