Moody’s RMS, CoreLogic Add to Modelers’ Take on Milton Insured Losses

Moody’s RMS has pegged private insured losses from Hurricane Milton to between $22 billion and $36 billion, with a best guess of $26 billion.

The Newark, California-based catastrophe modeler also narrowed its range for insured losses from hurricanes Milton and Helene to between $30 billion and $50 billion from wind, storm surge, and rain-induced flooding. The firm had earlier released a range of $35 billion and $55 billion from both hurricanes combined.

“We were fortunate to avoid the ‘grey swan’ event that many feared when Milton tracked and made landfall south of the Tampa-St. Petersburg [Florida] metro area,” said Mohsen Rahnama, chief risk modeling officer at Moody’s, in a statement Oct. 17. “Still, the storm’s large swath of damaging winds, subsequent storm surge, and inland flood footprints affected key exposure areas throughout the state, which will undoubtedly make it one of the costliest hurricanes to impact west Florida.”

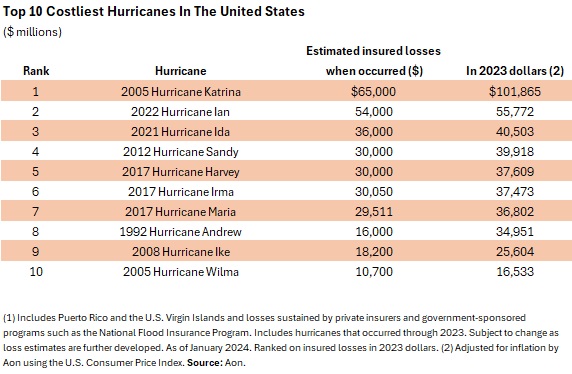

The range from Moody’s RMS also puts Milton in the top 10 costliest hurricanes to the insurance industry.

{kind=link}

Wind from Hurricane Milton—a Category 3 hurricane when it made landfall Oct. 9—caused nearly all of the losses ($21 billion to $34 billion), said Moody’s. Moody’s RMS said its range includes property damage and business interruption to residential, commercial, industrial, watercraft, and automobile lines of business, and considers post-event loss amplification since Milton and Helene happened so close in time. The firm also looked at losses from extended power outages as well as from tornadoes spawned by Milton.

Moody’s added it expects losses to the National Flood Insurance Program (NFIP) to exceed $5 billion from both Helene and Milton.

CoreLogic’s Take on Milton

Meanwhile, analytics firm CoreLogic on Oct. 17 chimed an insured-loss estimate for Milton of between $17 billion and $28 billion from wind and flood. The losses include damage to buildings, contents, and business interruption for onshore personal and commercial properties.

CoreLogic also said a majority of losses, $13 billion to $22 billion, will be from wind.

Milton struck Florida’s West Coast and traveled through the state to the Atlantic just two weeks after Helene affected many of the same areas, although it made landfall at Florida’s Big Bend and also impacted other southeastern states. Modelers have said there was some difficulty in assessing loss attribution between the storms. CoreLogic added that some properties, particularly in Tampa, were affected by storm surge during Helene and wind damage during Milton, creating “a scenario where leakage into wind-only policies is possible.”

A standard homeowners policy does not cover flood or storm surge.

Raj Vojjala, managing director of modeling and analytics at Moody’s, added, “It’s important to not just consider the overlap across areas affected by high winds and surge in Milton and Helene, but also areas that sustained damage during Hurricane Ian in 2022 that haven’t fully recovered yet.”

What Others Say

Estimates of insured losses from catastrophe modelers vary, and can include different variables.

Verisk came in with a high range for Milton of between $30 billion and $50 billion from damages caused mostly by wind. The range privately insured losses to onshore property due to wind, storm surge, and precipitation-induced flood. Verisk’s loss estimate does not include losses to the federal NFIP. Verisk added that its range also does not include litigation, inland marine, ocean marine cargo and hull, infrastructure, and loss adjustment expenses.

Fitch Ratings, in assessing the impact to the marketplace, also said it expected Hurricane Milton to cause between $30 billion and $50 billion in insured losses to push total industry losses in 2024 above $100 billion for the fifth straight year.

Karen Clark & Co, named after the mother of catastrophe modeling, issued a single number for insured losses: $36 billion. The estimate includes losses from wind, storms surge, and inland flooding to personal, commercial and industrial properties and vehicles, as well as business interruption.