US P/C Underwriting Results: Two Years in a Row Over $20 Billion in the Red

For the second year in a row, the U.S. property/casualty industry booked an underwriting loss of more than $20 billion primarily due to the lackluster performance of personal auto and home insurance lines.

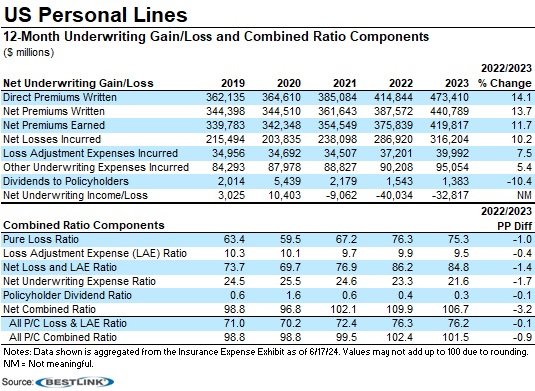

The total U.S. P/C underwriting loss in 2023 was about $21.6 billion compared to an underwriting loss of $25.8 billion the year prior.

According to a financial review of the industry by AM Best, homeowners/farmowners and private passenger auto insurance segments took an underwriting loss of $32.8 billion in 2023, which was actually an improvement from the $40 billion underwriting loss the pair of lines had in 2022.

Home and auto also logged an underwriting loss in 2021 (about $9.1 billion). Since 2021, home and auto have recorded combined ratios of 102.1, 109.9, and 106.7, respectively, as losses outpaced 11.7% growth in premiums earned in 2023.

{kind=link}

More weather-related events and higher repair costs have hurt each line, plus auto has dealt with higher medical costs and fatality rates. The duo has earned a negative outlook from the industry rating agency.

David Blades, associate director of industry research and analytics at AM Best, said most of the catastrophe losses paid out by home and auto insurers in 2023 were from secondary perils. Only one hurricane, Idalia, made landfall in 2023. The Atlantic hurricane season in 2024 has already seen the earliest ever Category 5 storm, and is expected to be extremely active.

Blades said personal lines carriers have been seeking rate increases but “regulatory constraints, inflationary pressures and more frequent and severe weather-related events continue to dampen results.”

AM Best said property reinsurance placements have recently gone smoother than prior renewal periods, but challenges in the market have caused higher retentions and co-participation levels for many primary insurers.

“The ability to absorb multiple events from primary and secondary perils, both financially and operationally, in a relatively short period of time is become even more important,” AM Best said.

Commercial lines saw underwriting income of about $10.3 billion in 2023, but that was nearly 30% lower than in 2022. The segment in the U.S. was supported by positive results in workers’ compensation, surety, and the combined results of professional liability, directors and officers, errors and omissions, cyber and other lines AM Best groups into the “other liability – claims made” category.

However, commercial auto and property lines have each recorded underwriting losses for each of the last five years. Most recently, commercial auto’s underwriting loss in 2023 widened to about $5.2 billion. Commercial property booked an underwriting loss of nearly $1.5 billion, an improvement from a loss of about $2.2 billion in 2022, $5 billion in 2021, and about $6 billion in 2020.

AM Best has tagged commercial auto with a negative outlook as rate increases and expense cuts haven’t been enough to combat economic and social inflation. The line’s 2023 combined ratio was 109.2.

U.S. commercial property maintains a stable outlook, as premium growth of around 20% exceeded incurred losses and loss adjustment expenses.