US D&O Insurance Segment’s Improved Results Unlikely to Be Sustainable: Fitch

The U.S. directors and officers (D&O) liability insurance segment’s strong underwriting profit of 2023 is unlikely to be sustainable, according to Fitch Ratings in a report.

Fitch attributed this reality to declining premium revenues from lower premium rates, as well as the segment’s inherent underwriting volatility related to changes in litigation activity, defense costs and settlement trends.

Given the increased competition seen in the sector, Fitch said, “softening market conditions are anticipated to prevail for the third consecutive year in 2024.” The ratings agency cited Aon’s fourth quarter D&O market survey, which indicates D&O primary renewal rates have dropped in the last seven consecutive quarters since Q4 2017.

“Pricing pressure remains more pronounced in higher-layer and excess business, given abundant underwriting capacity,” according to Fitch in its report, titled “U.S. Directors and Officers Liability Market Update.”

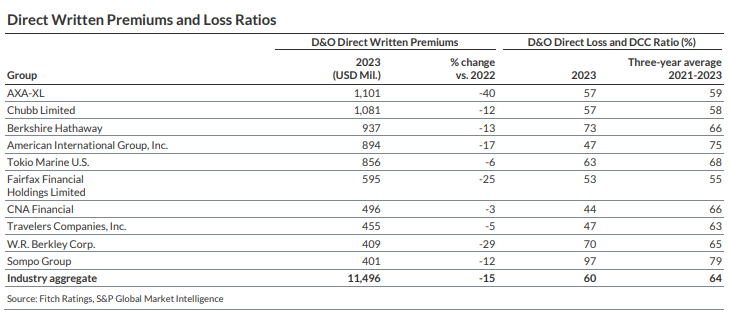

But the good news is that the U.S. D&O segment posted favorable statutory underwriting performance in 2023 for the third consecutive year, Fitch said, noting that the loss and defense and costs containment (DCC) ratio improved by 8 percentage points in 2023 to 60.4%, the best result since 2014.

{kind=link}

Fitch said D&O statutory direct written premiums (DWP) declined by 15% in 2023, following a 9% fall in 2022, reflecting weaker segment pricing. Direct earned premiums declined at a slightly lower 12% in 2023 and totaled $12.7 billion.

In response to poorer market performance in 2017-2020, industry DWP increased by 134% during the period 2018-2021. “However, a return to operating success has fostered a shift in pricing momentum, leading to a 23% DWP decline from 2021-2023 to $11.5 billion. Premium volume is likely to decline further in 2024.”

Class Action Filings

Fitch said that securities class action activity, which is typically connected “to allegations of accounting irregularities, misleading financial statements or earnings guidance, or regulatory compliance issues, remains a prime source of D&O claims. Class action activity reached record levels in 2017-2019 due in part to a rash of merger objection claims.”

During 2020, the number class action filings dropped during the coronavirus pandemic — particularly for merger objection claims, Fitch noted. However, the volume of more traditional class actions rose for the first time in three years in 2023, said Fitch, quoting reports published by NERA Economic Consulting Inc.

“While merger filings remain limited, traditional class actions are now gradually increasing as judicial activity moves towards prior norms, creating incremental exposure for D&O writers,” said Fitch in its report.

Future Risk Exposures

“The D&O market is exposed to several developing risks outside of traditional claims sources.” Fitch pointed to growing regulatory and compliance obligations which expand the potential for litigation such as: cyber risks; health and safety risks; environmental, social and governance (ESG) practices; climate risks, and employment practices.

“In late-December 2023, the SEC rules for cyber disclosures took effect that require publicly traded companies to file a disclosure within four business days of determining that a material cyber event has taken place,” said Fitch. “Since the cyber event is likely to still be continuing there is the potential for misstatements, which could be material and resulting in future litigation.”

D&O Company Market Share

Fitch said that market share of companies writing D&O remained unchanged in 2023. AXA-XL continues to be the leading U.S. D&O writer with a 9.6% market share, followed by Chubb (9.4%), Berkshire Hathaway (8.1%), AIG (7.8%) and Tokio Marine US (7.4%).

The larger companies that gained market share in 2023 due to a smaller decline in premium volume versus peers include CNA Financial, which moved to seventh largest (with a 4.3% market share) from eighth a year earlier, and Travelers eighth (4.0%), moving from 11th largest in 2022.

“Among the top 10 writers in the segment, companies with the best 2023 direct incurred loss and DCC ratio were AIG, CNA Financial and Travelers, with each posting a below 50% result.”