Increased Vehicle Sales, Search for Lower Rates Boost Auto Insurance Shopping

Auto insurance shopping rates rose 12% year-over-year in the second quarter of 2023, according to a new TransUnion report.

While vehicle sales played a role in the increase, TransUnion said in a press release that the search for lower insurance premiums was the primary driver. The consumer price index for motor vehicle insurance rose 17% in June 2023 compared to June 2022.

These findings are detailed in TransUnion’s latest quarterly Insurance Personal Lines Trends and Perspectives Report, which highlights trends in the auto and property insurance industries as well as survey data about consumers’ behaviors and attitudes.

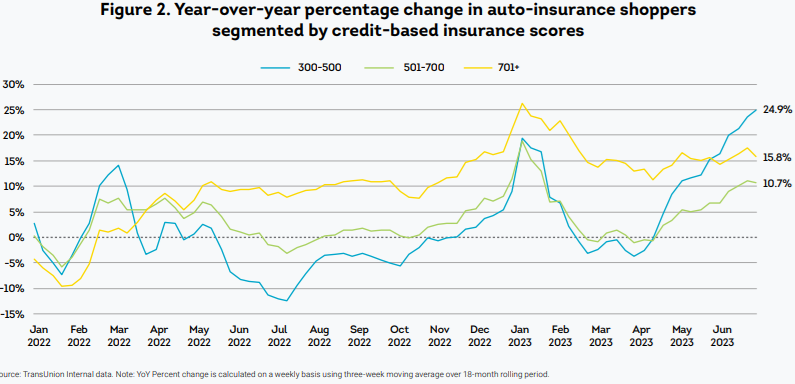

Growth Across All Credit-Based Insurance Score Groups

Despite historically high vehicle prices and increased auto insurance premiums, J.D. Power’s US automotive forecast for June 2023 estimated a 23% boost in new vehicle sales year-over-year. Meanwhile, used car sales dipped slightly because of improved new vehicle inventory.

“There was a drop in shopping activity among riskier consumers in Q2 2022, partly due to insurers’ reduced marketing spend; however, we saw a rebound in activity from that segment in Q2 2023,” said Stothard Deal, vice president of strategic planning for TransUnion’s insurance business. “Lower risk consumers have been consistently shopping at higher rates for the past 12 months.”

{kind=link}

Property Insurance Shopping Slows But Remains Elevated

The report found that homeowners are also shopping for lower rates, with property insurance shopping among that group rising 13% in Q2 2023 compared to the same time last year. However, the shopping rate was down 7%, compared to Q1 2023, most likely due to increasing interest rates and stubbornly high home prices.

TransUnion said this presents potential challenges and opportunities for insurers with Gen Z and Millennial customers. As these groups are priced out of homeownership, some may opt to live in regions more prone to natural disasters, which has significant implications for insurance losses. Others may simply choose to continue renting, which opens an opportunity for insurers to modernize their renter’s insurance offerings, TransUnion wrote.

“It’s time for insurers to start thinking about how to most effectively engage with their upcoming Gen Z customers,” Deal said. “We know they are more likely to learn about new products and services from social media and appreciate receiving personalized offers.”

A New World of Risk for Drivers and Insurers

In its full report, TransUnion warned that a possible factor contributing to profitability challenges is the deterioration of driving behavior. The company reported that in the early days of the pandemic, overall vehicle miles traveled plummeted. They have since returned to pre-pandemic levels. At the same time, however, moving violation rates are still down nearly 13% vs. the pre-COVID-19 annual average.

“While that may sound like good news, a look at the details reveals a different story,” the report reads. “Fatal accidents are at their highest level in decades — 22% higher than pre-COVID-19 averages. Fatalities resulting from alcohol impairment, speeding and failure to wear a seatbelt are all up by approximately 20%.”

TransUnion reported that moving violations are down not because of a change in driving behavior, but because of changes in traffic enforcement. Insurance carriers typically use these violations to add surcharges to the premiums of risky drivers. With fewer violations since 2020, though, TransUnion estimates the auto insurance industry has lost an estimated $200 million per year in lower premium capture that will be made up by an increased rate burden landing on all drivers.

Driver sentiment is changing, too. According to the TransUnion Q1 2023 Insurance Consumer Survey, 35% of Gen Z drivers feel that wearing a seat belt isn’t necessary for short trips, and 30% of Millennials think speeding is acceptable — both higher rates than in older age groups.

Insurers Implementing Mitigation Strategies, Consumer Landscape Evolving

TransUnion predicts the insurance industry will continue to react to profitability challenges.

“As insurers seek rate adequacy through price increases, they are taking short-term loss mitigation actions, including limiting distribution channels, strengthening underwriting on new business, selling policies only as part of a multi-line bundle or even withdrawing from some geographic markets,” the report reads.

Meanwhile, the company reported that consumers will continue to shop as rates increase, though the mitigation strategies referenced above “could make switching more difficult.” The company believes the consumer landscape will evolve as more members of Gen Z age into credit-active adulthood and increasingly seek home and auto insurance.