Berkshire’s GEICO Posts 2021 Profit Much Lower Than 2020

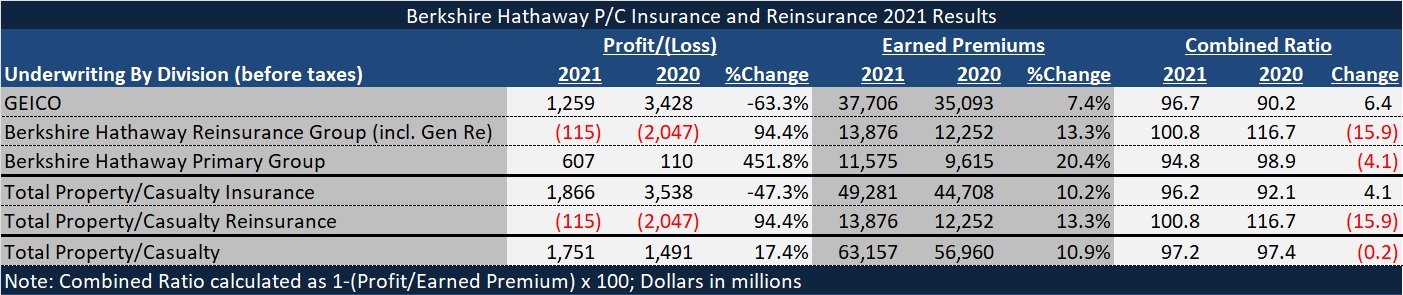

Although Berkshire Hathaway’s biggest insurance operation GEICO reported a 63 percent drop in pretax underwriting income in 2021, overall the conglomerate’s insurance and reinsurance operations saw pretax underwriting profit jump nearly 12 percent, the annual report reveals.

Underwriting profit for Berkshire’s primary commercial insurance operations almost returned to levels recorded during 2014-2018, and underwriting losses came in lower for Berkshire’s reinsurance operations in 2021 than in recent past years, bringing the overall combined ratio for all of Berkshire’s property/casualty operations to 97.2, nearly in line with last year’s combined ratio. (Editor’s Note: For the purposes of this article, CM editors approximated the combined ratio calculation using underwriting earnings and earned premiums presented in the annual report.)

{kind=link}

On Saturday morning, Berkshire released its fourth-quarter 2021 and full-year 2021, along with Chair Warren Buffett’s annual letter to shareholders.

Buffett didn’t say much about insurance in his annual letter, although he did list the insurance operations as the first of “four giants” that account for a “large chunk” of Berkshire’s value. (Other giants are BNSF Railroad, Berkshire Hathaway Energy and Berkshire’s stake in Apple.)

“The product will never be obsolete, and sales volume will generally increase along with both economic growth and inflation. Also, integrity and capital will forever be important,” he said, referring to insurance.

“There are, of course, other insurers with excellent business models and prospects. Replication of Berkshire’s operation, however, would be almost impossible,” he wrote.

Like other auto insurers, GEICO reported a record year in 2020, and 2021 underwriting results that were worse than pre-COVID levels of 2019. In 2020, in spite a six-month program of COVID-related premium givebacks totaling $2.9 billion from GEICO to its policyholders, the carrier reported $3.4 billion of pretax underwriting profit. The 2020 profit, resulting from lower auto claim frequencies, translated into a 90.2 combined ratio for all of 2020—lower than it had been in the decade of results that Carrier Management has tracked for Berkshire Hathaway.

In 2021, written premiums increased $3.5 billion (to $38.4 billion), or 9.9 percent, compared to 2020 but losses and loss adjustment expenses increased $5.0 billion, or 19.1 percent, pushing the loss ratio up more than 8 points.

“Claims frequencies in 2021 were higher for all [personal auto] coverages,” the Management Discussion and Analysis section of the latest annual report said, citing bodily injury and property damage frequency jumps in the 13-14 percent range, and collision frequency increases of over 20 percent. Reporting that claim severities were up as well, the report also disclosed a $1.8 billion takedown in prior-year reserves impacting GEICO’s loss ratio in the other direction (roughly 4.8 points based on $37.7 billion of earned premiums).

Adding underwriting expenses to the equation, GEICO’s combined ratio for 2021 was 96.7—more than 6 points higher than the 2020 combined ratio and about one point higher than 2019.

The underwriting profit story was more positive a Berkshire’s other primary insurance operations—the commercial and specialty operations that include Berkshire-Hathaway Specialty, MedPro Group, and USLI, among others. Overall written premiums jumped 23.3 percent for these companies, with Berkshire Hathaway Specialty recording the biggest jump—36 percent.

Although the Berkshire report does not break out underwriting profit figures by company for this commercial lines group, together the combined ratio for Berkshire Hathaway Primary Group was 94.8 in 2021—about 4.0 points lower than 2020, and 1 point lower than 2019—producing a pretax underwriting profit of $607 million.

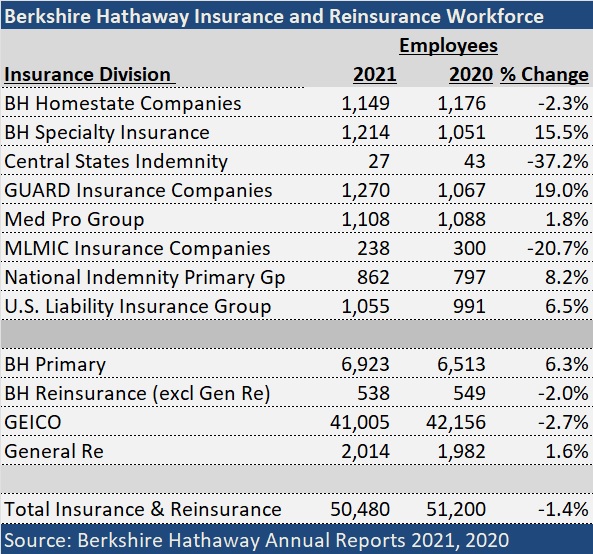

The report does include a breakdown of the workforces of all the insurance and reinsurance operations, which indicates that Berkshire Hathaway Primary Group bucked an industrywide trend, increasing staffing by more than 6 percent. GEICO and the reinsurance operations reported declines in headcount in 2021.

{kind=link}

The Bottom Line

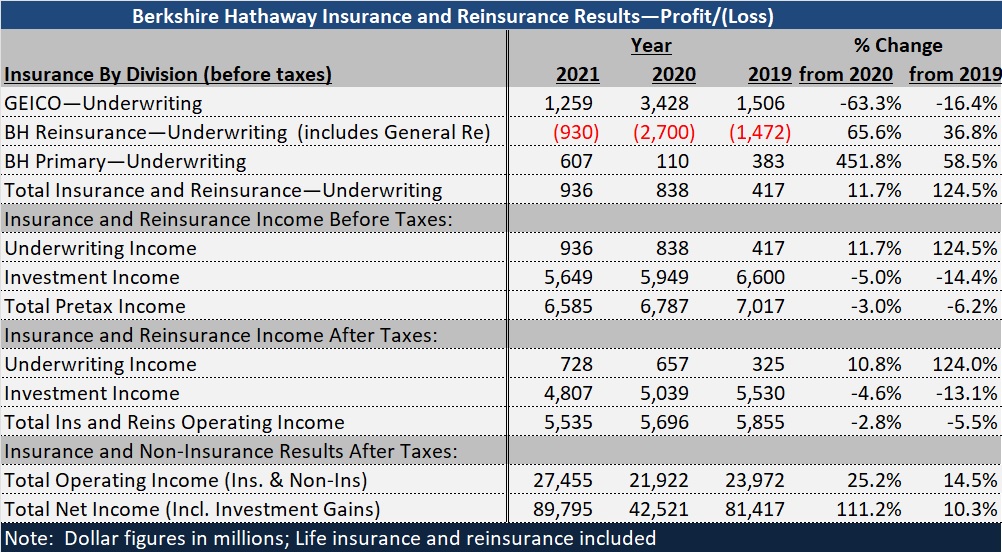

Pretax underwriting results for the property/casualty businesses are set forth in the first chart of this article, including results for P/C reinsurance and retroactive reinsurance operations. While Berkshire posted $667 million in pretax underwriting profits for P/C reinsurance, $782 million of underwriting losses for retroactive reinsurance operations brought the total to $115 million written in red ink.

Life reinsurance operations suffered bigger underwriting losses bringing total pretax underwriting losses for all reinsurance operations to almost $1 billion ($930 million to be exact).

Combining all the P/C and life insurance and reinsurance operation results, after-tax underwriting profit landed at $728 million in 2021, up 10.8 percent from 2020.

Investment income for the insurance operations, however, is the bigger driver of overall operating results, and with investment income falling 4.6 percent to $4.8 billion, overall operating income for the insurance and reinsurance operations fell 2.8 percent to $5.5 billion.

{kind=link}

Bottom-line net income for insurance and non-insurance operations more than doubled, reaching $89.8 billion. Most of the jump, however, was attributable to investment gains, with after-tax operating income for insurance and non-insurance operations rising 25.2 percent to $27.5 billion.

Photograph: (AP Photo/Nati Harnik)