Europe Reinsurers’ H1 Profits Climb on Lower COVID Claims, Hardening Prices: Moody’s

The four largest European based reinsurers – Munich Re, Swiss Re, Hannover Re and SCOR – reported sharply higher profits in the first half of 2021, compared with the same period in 2020 — as a result of lower COVID-19 claims and hardening property/casualty prices, according to a report published by Moody’s.

The four major reinsurers reported aggregate net profit of €3.6 billion ($4.2 billion) in the first six months of 2021, up from €200 million (US$234.3 million) a year earlier, said Moody’s Investor Service in a report on the four reinsurers, published on Aug. 18. “The significant jump reflects the depressed results last year, affected by turmoil in the financial market and the first wave of COVID-19 claims, but also improving underlying conditions.”

Underlying combined ratios recovered significantly in H1, reflecting premium and rate increases at recent renewals, added the ratings agency. Indeed, P/C reinsurance underwriting profits were strong with the four reinsurers reporting combined ratios (costs and claims as a percentage of premiums) of between 94% and 97%, down from figures north of the 100% break even point in the first half of 2020 when they saw high coronavirus-related claims, which have since abated. (Combined ratios below 100% indicate underwriting profits).

“The underlying improvement of all four reinsurers’ underwriting profitability reflects positive pricing trends that began in 2020,” said Moody’s.

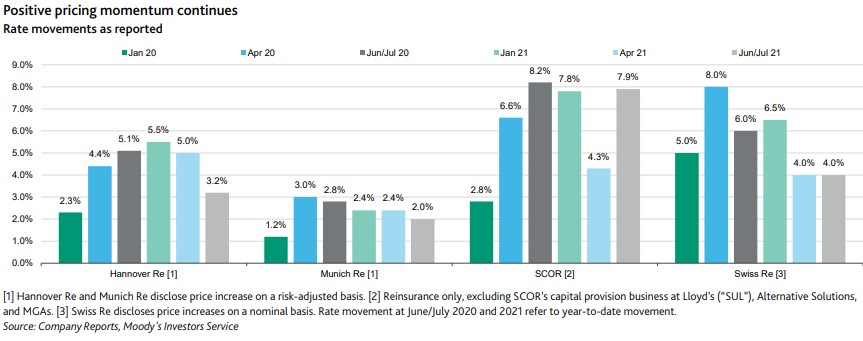

P/C Prices Continue to Harden

All four reinsurers reported positive price momentum in the June/July policy renewals, although increases were more moderate than earlier this year and in 2020, said Moody’s. (See graphic below).

{kind=link}

“A combination of persistently low interest rates, rising loss cost trends, and better modeling of so-called secondary perils – less severe but more frequent natural catastrophes such as wildfires – will also support price increases over the next 12-18 months, although they will likely be more moderate than in 2020 and early 2021,” the report continued.

Overall, reinsurers have taken advantage of the positive pricing environment to grow their premiums, but Moody’s said growth rates vary as a result of different underwriting policies.

In H1, growth rates in reported gross premiums written ranged from 5.5% for Swiss Re to 15.5% for Munich Re, with Hannover Re (11.9%) and SCOR (7.1%) in between.

Hannover Re and Munich Re reported the strongest growth because they have consistently expanded their books during renewals over the last 18 months, while SCOR and Swiss Re refrained from growing their books overall in 2020 because they were repositioning their portfolios. Moody’s said that SCOR and Swiss Re therefore will have to wait longer to benefit from recent price increases.

Diminishing COVID-19 Claims

COVID-19 related losses continued to weigh on the group’s H1 results, although less than in the same period a year ago. On aggregate, since the beginning of the pandemic, the four reinsurers have reported, €9.6 billion ($11.3 billion) of COVID-related reinsurance claims (net of retro reinsurance). These figures include paid claims, case reserves and incurred but not reported (IBNR) reserves, said Moody’s.

The companies reported moderate additional pandemic-related P/C claims in 2021, and reserves set aside for 2020 COVID-19 claims mostly have held up well, said Moody’s. SCOR was the exception, however, because it had to strengthen its reserves against prior business interruption claims, due to adverse court decisions in France and the UK, as well as new claims for two separate lockdown induced events, said Moody’s

After the industry re-evaluated many property policies and excluded pandemic coverage from business interruption coverage, there were only minimal additional claims in these lines of business, said Moody’s, noting, however, that event cancellation policies, where Munich Re has significant exposure, continue to generate new losses.

“As reinsurers typically underwrite event cancellation risk years ahead of the event, this is in line with expectations,” the ratings agency explained.

Mortality Claims Exceed Expectations

While the four reinsurers reported relatively low pandemic-related P&C reinsurance claims, mortality claims in the second quarter were higher than anticipated. These claims were mainly driven by significant mortality in India and in South Africa. Conversely, mortality claims in the key U.S. market were largely in line with expectations, confirmed Moody’s.

“Reinsurers’ mortality risk is concentrated in the U.S., which will remain the main determinant of future pandemic-related losses. However, developments in Q2 demonstrate that severe excess mortality in developing markets, where vaccination rates are very low, can have a significantly negative impact on technical margins.”

H2 Catastrophe Activity

Following already significant natural catastrophe activity in H1, claims from a number of large events in July will negatively affect reported P/C reinsurance profitability in the third quarter, said Moody’s, which explained that P/C reinsurance underwriting results tend to weaken in the second half of the year during the north Atlantic hurricane season.

“However, claims related to heavy flooding in Europe and China, civil unrest in South Africa, and a the risk of an active hurricane season, will likely put some pressure on the four large reinsurers’ operating performance in the second half.”

As a result, Moody’s expects combined ratios to increase in the second half, “indicating a deterioration in P/C underwriting profitability.”

Source: Moody’s Investor Service