AXA, Other Mega-Investors Seek to Avoid Portfolios with Global Warming Potential

All good money managers expect to outperform their benchmark, and by one such metric the French insurer and investor AXA SA recently scored a market-beating success. Not by delivering higher returns, but by generating a lower level of global warming.

If human activity is driving carbon emissions and temperatures to dangerous highs, then a giant asset owner like AXA with a 650 billion-euro ($790 billion) horde of stocks, corporate bonds and sovereign debt is one of the principal proprietors of climate change. In theory, that means every investment portfolio can be evaluated for the “warming potential” of its underlying assets.

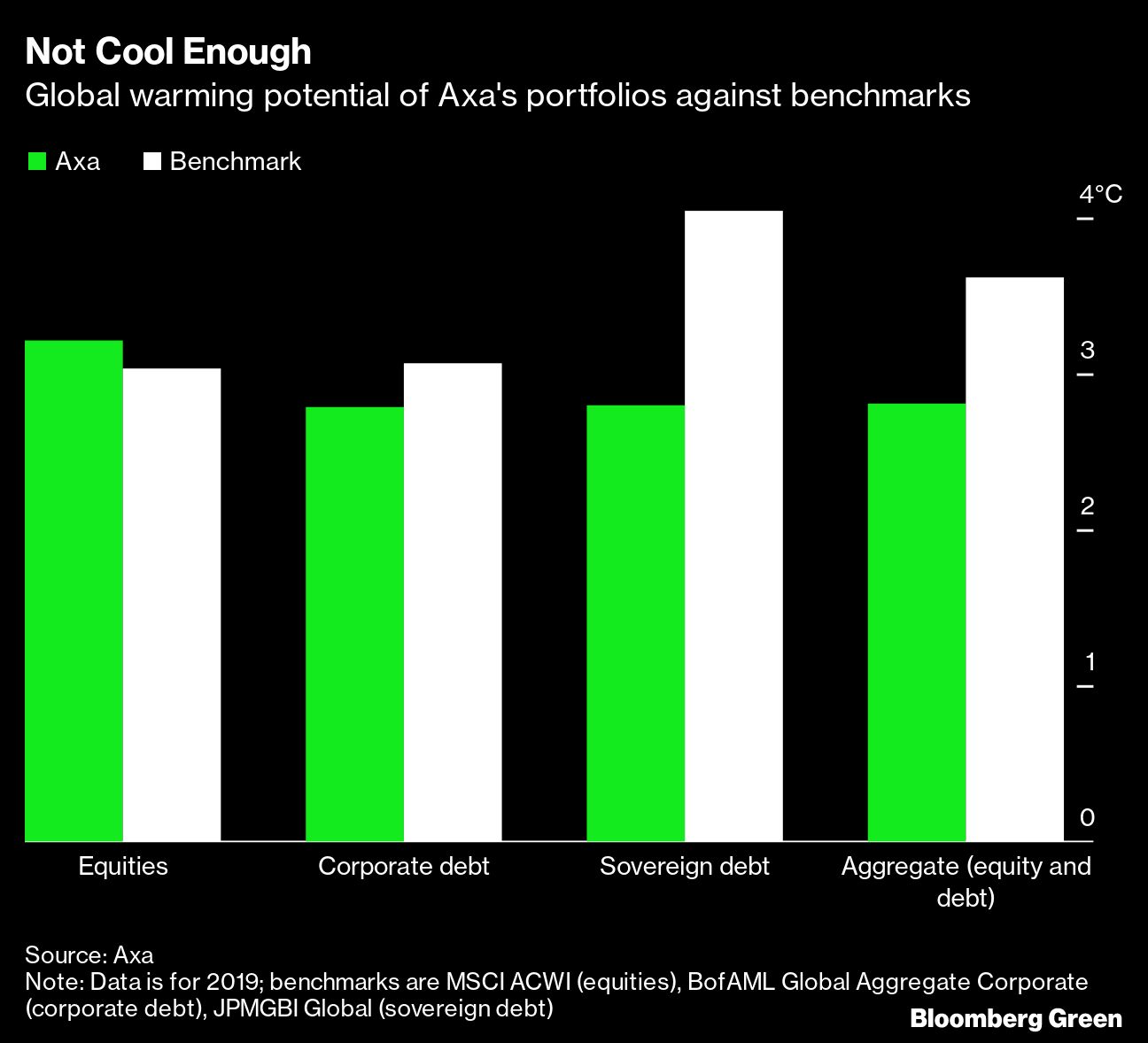

After a painstaking process of self-evaluation that took two years, including a significant shift away from heavy polluters, AXA concluded its assets would warm the planet by 0.8 degrees Celsius less than if it held all the companies in major global stock and bond indexes. That was good news for an early adopter of portfolio-warming metrics.

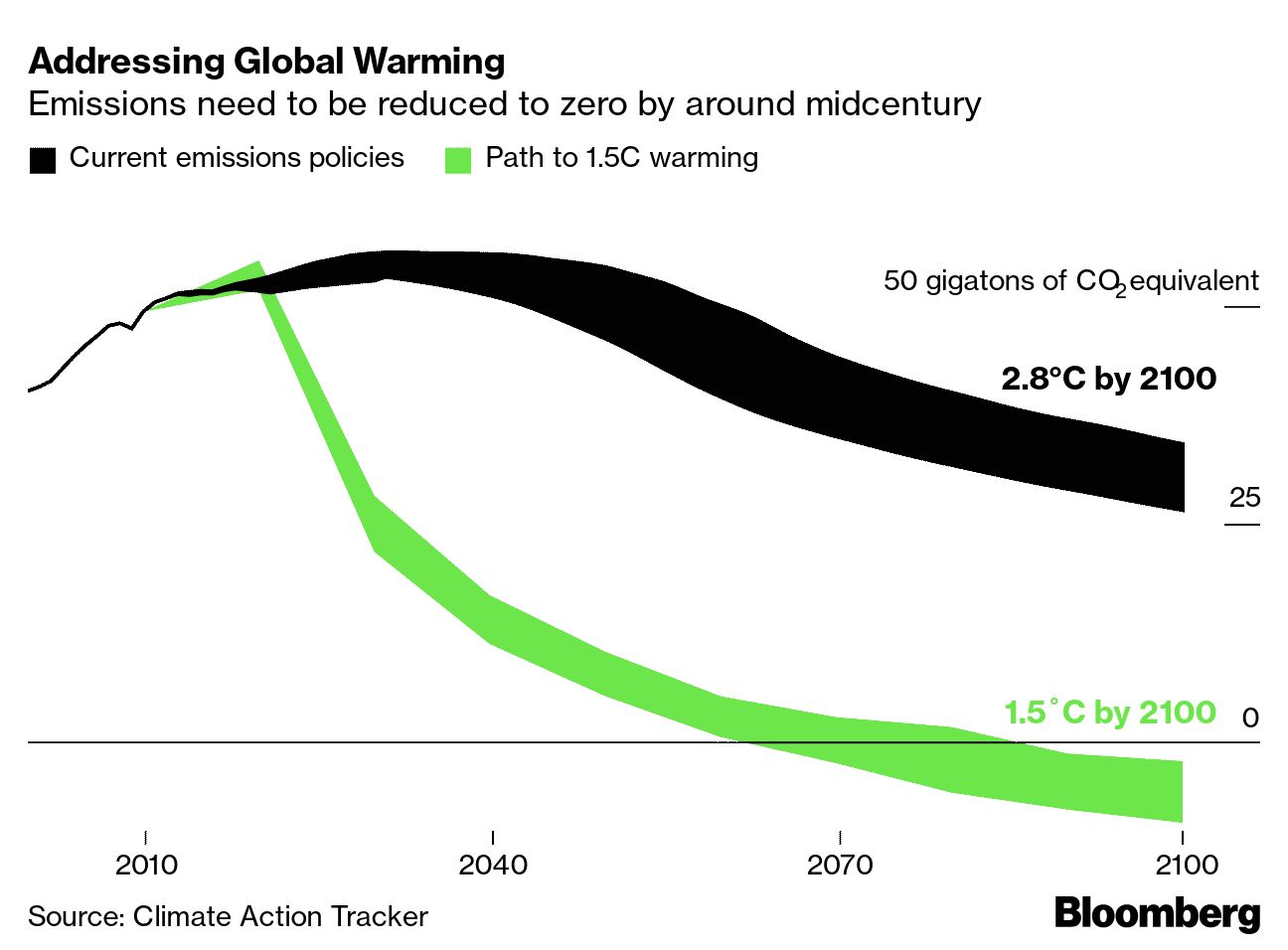

The bad news: AXA’s portfolio implied a temperature increase of almost 3°C above pre-industrial levels by 2100. At that level, scientists warn of mass extinctions of animal species, large parts of the planet becoming uninhabitable due to extreme heat, rising sea levels swallowing up coastal cities, and lush rainforests turning into savannas. It also would put AXA, despite its climate-conscious efforts, on the wrong side of the 2015 Paris Agreement in which every nation agreed to limit warming to 2°C.

{kind=link}

“You can try to drive your portfolio to a cooler temperature, but when you have to operate in an investment universe that is really trapped in a rising carbon footprint, you will encounter strong limitations on what you can do,” said Ulrike Decoene, AXA’s head of corporate responsibility. “We’re not seeing the broader economy decreasing its warming potential and that’s worrying.”

And it’s not only AXA that’s taking the temperature of its assets. UK insurer Aviva Plc and Japan’s $1.7 trillion Government Pension Investment Fund have published data on warming potential. New York-based BlackRock Inc., with $8.7 trillion of assets, plans to do the same for some of its funds. The practice is likely to spread in the years ahead.

There’s big promise in taking warming potential seriously. The world’s largest money managers, with holdings in every major company, might be better suited than a single government to gauge the rate at which businesses are warming the planet. These temperature readings can then help giant investors prod the companies to cool things down more quickly, fulfilling the promise of the sustainable investing movement.

But the process of avoiding the apocalypse can look quite alarming, especially when those managing trillions in assets discover they own a 3°C future. If even climate-conscious pools of capital are flashing such doomsday warnings, can this kind of data really help avoid catastrophic warming?

The dire outlook has prompted hundreds of banks, insurers and other corporations to unveil net-zero emissions targets as concerns about the environment breach the walls of the capitalist establishment and force companies to change the way they conduct their business. Paris-based AXA has done more than most in the financial-services industry to reckon with its impact on the planet.

Ranked among Europe’s largest insurers, AXA stopped underwriting certain new coal projects in 2017 and last year committed to wind down its existing coal insurance contracts by 2040. At the same time, the company has been divesting its coal and oil sands holdings since 2015 and pledged two years ago to put 24 billion euros into green projects by 2023. Perhaps most ambitiously, AXA has committed to reduce the warming potential of its portfolios to 1.5°C by 2050.

Yet all of these efforts, some pursued for years, have barely budged the temperature of its overall asset pool. From the start of 2018 through the end of 2019, AXA’s holdings cooled by just 0.2°C to 2.8°C. The warming potential metric for 2020 will be published by June; AXA declined to provide guidance.

Decoene said the slight reduction followed divestments from the most carbon-intensive sectors, with the average warming potential of companies on its exclusion list at 4.6°C. Going forward, AXA is committed to reducing the carbon footprint of its equity, corporate debt and real estate investments by 20% by 2025, she said.

Calculating the implied temperature of a portfolio is a relatively novel concept, and there’s no consensus on the best way to do it. Some critics question whether it’s even possible to make an accurate forecast.

{kind=link}

A report co-authored last year by David Blood, who started sustainable investing firm Generation Investment Management with Al Gore, found at least seven different methods of measuring portfolio alignment from firms including MSCI Inc. and a unit of S&P Global Inc. That may lead to investor confusion, and even increase the risk of greenwashing, “as the metric could be adjusted to fit different purposes,” according to the paper.

AXA collaborated with a Swiss fintech company called Carbon Delta, which has since been acquired by MSCI, to develop a methodology. AXA was more open to experimenting with climate metrics than many of its global peers, in part because of pressure from the French government. There’s also growing interest among the company’s clients to show how their businesses stand up next to the goals of the Paris accord. The process is complicated.

An investor’s portfolio has the same warming potential as everything inside of it. That means AXA needed to determine just how much it believed each of its assets would increase global temperatures by the year 2100. Climate scientists do this type of modeling using what’s known as temperature pathways, projecting different scenarios for the coming decades based on assumptions about greenhouse gas output. Will society’s adoption of electric vehicles go faster than expected? Will coal power plants continue operating for longer?

AXA needed to form the same assumptions about the future emissions associated with everything in its vast portfolio, from U.S. treasuries to Nestle SA. To do that, it needed reliable data on emissions—both those produced directly by a business or a country, as well as those created by customers using the products of a company whose shares it owns. Emission-reductions plans, such as net-zero pledges or corporate investments in green technologies, as well as relevant state-level commitments to cut greenhouse gases, also are taken into consideration.

With all that information, AXA’s portfolio can be assessed under the same sort of temperature pathways used by scientists to estimate how much carbon dioxide can be emitted by the economy before the planet breaches various warming thresholds. That’s how AXA calculates its portfolio score, based on the size of its holdings.

At a company level, the results of this process can be surprising. Even companies making bold commitments to reduce emissions can heat up a portfolio. Amazon.com Inc. plans to be carbon neutral by 2040, for example, and yet MSCI ESG Research LLC ascribes a warming potential of 3.9°C to the retail giant. Apple Inc.’s 2.9°C warming score stands at odds with its pledge to zero-out emissions from its supply chain and products by 2030. By that year, Microsoft expects to be carbon negative, meaning it plans to be removing greenhouse gas from the atmosphere on balance; it gets a 2.1°C score.

And giant tech companies tend to be forthcoming with emissions data, which isn’t the case in other sectors. A new report by the Transition Pathway Initiative determined that only 16 of 111 large publicly listed industrial companies, such as miners and steelmakers, publish emissions projections that align with the Paris Agreement.

Still, even with imperfect data and subject to a fair amount of skepticism, the effort to calculate warming potential shows how climate concern is changing the rules of the game for investors and businesses alike. Measuring a company’s alignment with the Paris objectives has the potential to become a regular part of investment analysis, in much the same way fund managers now scrutinize cash flows and earnings.

“It would be ideal if this metric became part of the everyday lexicon of traders and analysts,” said David Lunsford, co-founder of Carbon Delta who now leads climate strategy and policy at MSCI in Zurich. “More data disclosure would help us to thoroughly assess companies’ temperature alignments and could encourage a wider adoption of the metric.”

Investors that have published a warming potential calculation have two notable commonalities: Their portfolios imply around 3°C of warming, and they have concluded there’s only so much cooling possible on their own.

“To some extent, our portfolio reflects the real economy and there’s a limit to which we can disconnect from that,” said Ben Carr, an analytics and capital-modeling director at Aviva, where he has led the London-based insurer’s work on the development of climate metrics. Aviva recorded a warming potential at the end of 2019 of 3.2°C for its equities holdings and 3°C for corporate credit.

For most of the early adopters, the results are rather dystopian. Japan’s GPIF estimated 2.76°C of warming for equities and 2.88°C for bonds in its home market, while its foreign stock and fixed-income holdings had a warming potential of 2.97°C and 2.76°C, respectively.

In the U.S., meanwhile, the California Public Employees’ Retirement System said its global equity and fixed-income holdings, which account for 75% of its assets, are on track for a warming potential of 3.23°C by 2050.

Aviva reduced the warming potential of its equity and credit portfolios by 0.2°C between 2018 and 2019 by engaging with portfolio companies. It also divested from those “where we see no prospect of progress,” Carr said.

While that approach may have brought some success in the past, time is running out to curb emissions and set the economy on path to net zero, according to a December report from MSCI’s ESG research group. Institutional investors, working with governments and the public, are going to have to do their part to persuade companies to make radical changes. If they don’t, there’s a growing risk that money managers will face a rapidly shrinking universe of investments that can be considered Paris-aligned, the MSCI analysts said.

Just 16% of an MSCI index covering 9,000 stocks globally were aligned to a 2°C temperature-rise scenario at the end of November, and only 5% were on course for a 1.5°C world, MSCI said, making clear just how much more needs to be done.

“The warming-potential concept requires a far broader public-private effort that cannot be achieved by investors alone,” said Decoene, who’s also responsible for corporate communications and brand management at AXA. “This is a huge undertaking, for us and also for markets, businesses and policymakers.”

World leaders will gather later this year in Glasgow, Scotland, for what could be the most consequential moment for climate diplomacy since the Paris agreement: a United Nations conference at which signatories of the 2015 accord are expected to ramp up their ambitions for cutting emissions.

The event in Glasgow also may be a significant moment for financial markets. Former Bank of England Governor Mark Carney, who was appointed UN Special Envoy for Climate Action and Finance in 2019, has laid out a strategy for building a net-zero world in which every financial decision is made with consideration for the climate. Among his desired outcomes is the development of a portfolio-alignment framework that investors can use to gauge where they stand on the path to net zero.

Currently, opinion is divided. The two co-chairs of the Transition Pathway Initiative, an entity supported by the likes of Pacific Investment Management Co. [PIMCO] and UBS Group AG that assesses companies’ preparedness for the transition to a low carbon world, offered a scathing criticism of implied temperature-increase metrics last month. Faith Ward and Adam Matthews said there’s a lack of reliable emissions data to make the computations and the metrics rely on assumptions.

By contrast, the Net Zero Asset Owner Alliance, a $5 trillion coalition of pension and insurance funds, including AXA, Aviva and Calpers, said this month it supports standardization and development of portfolio-warming metrics. Decoene said AXA, which leads the Alliance’s warming-potential working group, is aware of the weaknesses, but it’s still “actively promoting temperature metrics.”

The question of whether portfolio-alignment scores are informative or misleading forms part of a broader question about climate models. A recent paper by a group of academics and climate scientists suggests financial markets may misuse them because they operate on different time horizons and with different priorities, increasing the likelihood of mispricing climate risks and even greenwashing.

Generation Investment’s Blood warned against nitpicking. Even with flaws in the early models, warming-potential metrics can provide insight on the gap between a portfolio’s constituents policies and the goals of the Paris accord, he said.

“If we just continue with incrementalism, we aren’t going to get there,” Blood said. “We may need to rethink the allocation of capital. Perhaps climate impact needs to be the driver of that over the next five years. And perhaps we should debate the repercussions of a three-degree world.”

Action must be immediate and decisive to cut emissions, Blood said, and that should mean changes in the way investors make decisions. “If we have 10 years of great returns and yet are locked into a three-degree world, that is a terrible outcome for all our stakeholders,” he said. “Perhaps we should be measuring returns differently?”

Top photograph: Blast debris from a detonation rises at an open-pit coal mine. AXA stopped underwriting certain new coal projects in 2017 and last year committed to wind down its existing coal insurance contracts by 2040. Photo credit: Andrey Rudakov/Bloomberg.

Related:

- Lloyd’s Insurer Brit to Stop Insuring Australia’s Adani Coal Mine

- As Insurers Exit Coal Underwriting, They May Find It’s Good for Stock Valuations

- AXIS Capital Decides to Stop Insuring Arctic Oil and Gas Projects

- Lloyd’s Moves to End Insurance and Investments in Coal for Climate Sustainability

- Coal Financing Drying Up as More Countries Target Zero Carbon Emissions

- Climate Change Poses Much Greater Existential Risk for the World Than COVID-19